US stocks close the week with gains on the day. S&P and Nasdaq lower for the week.Next week will be the Grand Daddy of the earning calendar this quarterBaker Hughes oil rig count +5 to 482.ECBs Schnabel:Services inflation showing last mile in inflation fight especially difficultEuropean shares bounce back. Mixed performance for the week.Initial Atlanta Fed GDPNow growth tracker comes in at 2.8%University of Michigan consumer sentiment for July 66.4 versus 66.0 estimate (and prelim)Kickstart the FX trading day for July 26 w/a technical look at the EURUSD, USDJPY & GBPUSDUS Core PCE YoY for June 2.6% versus 2.5% estimateThe AUD is the strongest and the JPY is the weakest as the NA session begins.ForexLive European FX news wrap: A bit of respite ahead of the US PCE report

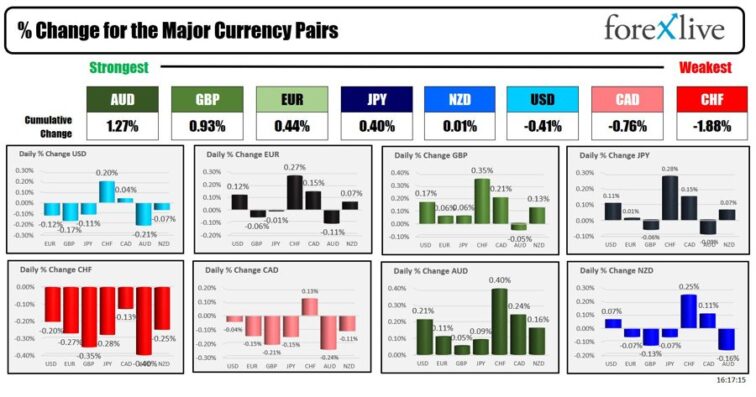

For most of the week, the flow of funds sent the JPY and CHF higher on flight to safety flows. The AUD (and NZD) lower as risk off sentiment dominated on the back of slowdown in China, lower commodities and stocks moving lower.

Today saw a reversal of some of those trends.

For the day, the AUDSD is the strongest of the majors. The CHF is ending as the weakest. The JPY is ending the day mixed. The USD which was mixed for a lot of the week is ending the week with the same fortunes today.

Stocks moved higher in both Europe and the US today.

The major European indices bounced back in trading today with all the indices higher.

German DAX, +0.68%France CAC +1.22%UK FTSE 100 +1.21%Spain’s Ibex +0.18%Italy’s FTSE MIB +0.12%

For the trading week, most of the indices were higher except Italy’s FTSE MIB

German DAX +1.38%France CAC, -0.22%UK FTSE 100, +1.59%Spain’s Ibex, +0.71%Italy’s FTSE MIB, -1.09%

The final numbers in the US closed the day with gains across the board.

Dow industrial average rose 654.27 points or 1.64% at 40,589.35.S&P index rose 59.86 points or 1.11% at 5459.09NASDAQ index rose 176.16 points or 1.03% at 17357.88The small-cap Russell 2000 rose to 37.08 points or 1.67% at 2260.06.

For the trading week, the results were mixed with the Dow up for the 4th consecutive week. The Russell 2000 was up for the 3rd week.. The S&P and the Nasdaq were down for the 2nd consecutive week. Next week will be influenced by a slew of earnings highlighted by Microsoft, Apple, Amazon and Amazon amongst other large cap titans in various industries.

US yields are closing the day near lows across the yield curve:

2 year yield 4.389%, -5.4 basis points5-year yield 4.0767%, -6.8 basis points10-year yield 4.195%, -6.0 basis points30-year yield 4.456%, -4.4 basis points

For the trading week:

2-year yield -13 basis points5-year yield, -9.4 basis points10-year yield, -4.7 basis points30-year yield, unchanged.

The 2-10 year rose by 8.3 basis points for the week to -19.4 basis pointe. The 2-30 year spread is ending positive by 6.7 basis points.

Fundamentally today, the PCE data was consistent with the PCE data from the GDP data yesterday.

The core PCE moved up by 0.188% (rounded to 0.2%. The YoY rose by 2.6%. The was unchanged from last month. The headline PCE rose of 0.1% (revised higher) with the YoY dipping to 2.5% from 2.6%.

The Michigan consumer survey data was mixed with the sentiment moving higher vs the preliminary, the current conditions lower and the expectations higher . Inflation results were more or less as expected and close to last months levels.

IN addition to the parade of earnings, the Fed, the Bank of England and the Bank of Japan will announce interest rate decision. The US jobs report will be released on Friday. Australia and EU CPI will be released. China PMI will be released as well.

Thank you for the support.this week. Wishing you all a great weekend (PS enjoy the Olympics).

This article was written by Greg Michalowski at www.forexlive.com.US stocks close the week with gains on the day. S&P and Nasdaq lower for the week.Next week will be the Grand Daddy of the earning calendar this quarterBaker Hughes oil rig count +5 to 482.ECBs Schnabel:Services inflation showing last mile in inflation fight especially difficultEuropean shares bounce back. Mixed performance for the week.Initial Atlanta Fed GDPNow growth tracker comes in at 2.8%University of Michigan consumer sentiment for July 66.4 versus 66.0 estimate (and prelim)Kickstart the FX trading day for July 26 w/a technical look at the EURUSD, USDJPY & GBPUSDUS Core PCE YoY for June 2.6% versus 2.5% estimateThe AUD is the strongest and the JPY is the weakest as the NA session begins.ForexLive European FX news wrap: A bit of respite ahead of the US PCE reportFor most of the week, the flow of funds sent the JPY and CHF higher on flight to safety flows. The AUD (and NZD) lower as risk off sentiment dominated on the back of slowdown in China, lower commodities and stocks moving lower. Today saw a reversal of some of those trends. For the day, the AUDSD is the strongest of the majors. The CHF is ending as the weakest. The JPY is ending the day mixed. The USD which was mixed for a lot of the week is ending the week with the same fortunes today. Stocks moved higher in both Europe and the US today. The major European indices bounced back in trading today with all the indices higher. German DAX, +0.68%France CAC +1.22%UK FTSE 100 +1.21%Spain’s Ibex +0.18%Italy’s FTSE MIB +0.12%For the trading week, most of the indices were higher except Italy’s FTSE MIBGerman DAX +1.38%France CAC, -0.22%UK FTSE 100, +1.59%Spain’s Ibex, +0.71%Italy’s FTSE MIB, -1.09%The final numbers in the US closed the day with gains across the board. Dow industrial average rose 654.27 points or 1.64% at 40,589.35.S&P index rose 59.86 points or 1.11% at 5459.09NASDAQ index rose 176.16 points or 1.03% at 17357.88The small-cap Russell 2000 rose to 37.08 points or 1.67% at 2260.06.For the trading week, the results were mixed with the Dow up for the 4th consecutive week. The Russell 2000 was up for the 3rd week.. The S&P and the Nasdaq were down for the 2nd consecutive week. Next week will be influenced by a slew of earnings highlighted by Microsoft, Apple, Amazon and Amazon amongst other large cap titans in various industries. US yields are closing the day near lows across the yield curve:2 year yield 4.389%, -5.4 basis points5-year yield 4.0767%, -6.8 basis points10-year yield 4.195%, -6.0 basis points30-year yield 4.456%, -4.4 basis pointsFor the trading week:2-year yield -13 basis points5-year yield, -9.4 basis points10-year yield, -4.7 basis points30-year yield, unchanged.The 2-10 year rose by 8.3 basis points for the week to -19.4 basis pointe. The 2-30 year spread is ending positive by 6.7 basis points. Fundamentally today, the PCE data was consistent with the PCE data from the GDP data yesterday. The core PCE moved up by 0.188% (rounded to 0.2%. The YoY rose by 2.6%. The was unchanged from last month. The headline PCE rose of 0.1% (revised higher) with the YoY dipping to 2.5% from 2.6%. The Michigan consumer survey data was mixed with the sentiment moving higher vs the preliminary, the current conditions lower and the expectations higher . Inflation results were more or less as expected and close to last months levels. IN addition to the parade of earnings, the Fed, the Bank of England and the Bank of Japan will announce interest rate decision. The US jobs report will be released on Friday. Australia and EU CPI will be released. China PMI will be released as well. Thank you for the support.this week. Wishing you all a great weekend (PS enjoy the Olympics).

This article was written by Greg Michalowski at www.forexlive.com. Read MoreNews

Forexlive RSS Breaking News Feed